Goals of this research paper are identifying factors of working capital management in small and medium enterprises; assessing methods and techniques that are being used to manage profitability and liquidity; analysing interdependence between working capital management and profitability and liquidity of SMEs. Because of weaker power, limited access to alternative forms of finance SMEs are less effective in working capital management. This study represents an attempt to learn more about SMEs` working capital practices and financial practices in particular. It adds extra knowledge and database to this area of finance and provides new questions to direct further research.

Importance of SMEs in Uzbekistan. SMEs are recognized as the driving force and the engine for economic growth in many countries. It produces essential goods and services, supplies jobs, delivers income for public sector, and creates and maintains infrastructure. Considering a role of small business in Uzbekistan concrete measures for support and stimulation of their further development consistently are being realized. Main of them are:

‒ Giving businessmen necessary rights and opportunities for performance of certain choice of activity, implementation of process of production and its transformation, a choice of sources, access to resources, product sales, establishment of the price, the order profit

‒ Possession of the property right to means of production, the made production and the gained income

‒ Creation of a certain economic environment and the socio-political conditions which are really providing a freedom of choice of a way of managing, possibility of investment

‒ Expansion of base of financing of business, increase of educational level and the qualified preparation

‒ Continuous improvement of legislative and regulatory base, existence of the tax privileges and the enterprise environment stimulating an enterprise initiative of society (N. Pardabekova, 2012).

In all, a total of 470 000 SMEs are registered in Uzbekistan (OECD, 2013; Karimova, 2012).

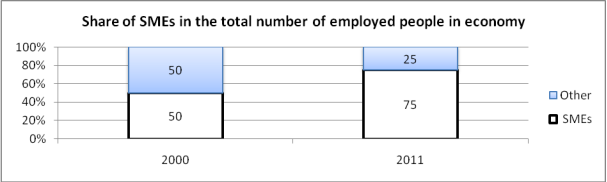

Fig. 1 [2]

The sector accounts for 75 % of total employment, 9 million people, in the country.

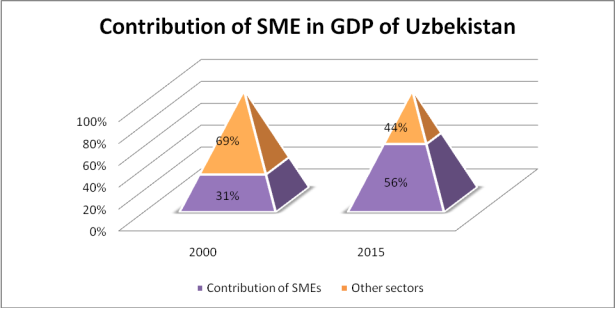

Fig. 2 [3]

In Uzbekistan the share of SMEs in GDP steadily increased from 30 % in 2000 to 56 % in 2015, which average world statistics are 55 % (Zokirov, 2015; OECD, 2013).

Realizing the importance of the private sector to the country’s development, the Government of Uzbekistan simplified tax system with unified flat rate of 13.2 % was introduced for small businesses in 2005, which replaced several types of taxes levied on different parts of activities. This rate has been reducing every year by the Government since then and for 2013 it is set at 5 % of gross revenue for manufacturing enterprises (Manzurova et al, 2012; Koraliev, 2014).

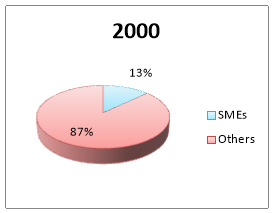

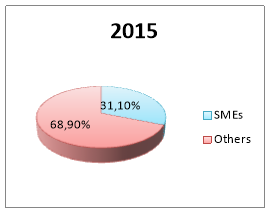

Fig. 3. Role of SMEs in production of goods in manufacturing sector in 2000 and 2015 years in Uzbekistan [3]

Also business registration procedures are also simplified by the Government, reduced the number of inspections of businesses conducted by various state authorities, reduced costs of obtaining various permits by up to three times, allowing private firms and especially SMEs to save money and time for regulatory compliance (UNDP, 2011).

However there are still regulatory and institutional constraints that affect productivity and competitiveness of SMEs.

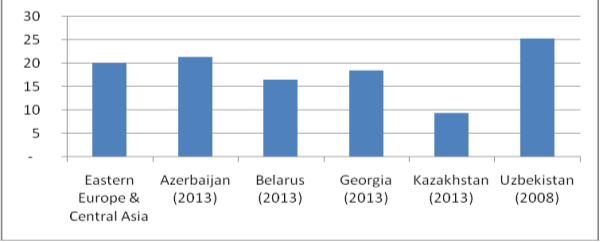

Fig. 4. Percentage of firms identifying access to finance as a major constraint [4]

As cross-country data from World bank report (2013) indicates that in Uzbekistan a major constraints towards access to finance are higher compared to other countries in the region.

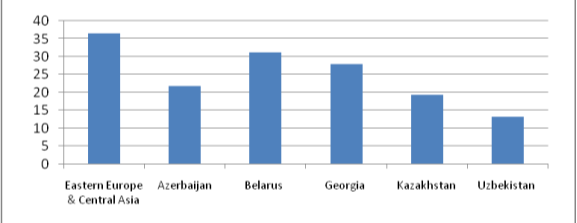

Fig. 5. Percentage of firms using banks for financing their investments [4]

In terms of underusing of financial services compared to peer countries, Uzbekistan holds leading position. Only 28.2 percent of surveyed firms in Uzbekistan reported having a bank loan or line of credit, and only 13.3 percent use banks to finance investments. Instead of relying on financial institutions, Uzbek enterprises are overwhelmingly self-financed (using earnings or borrowing from friends and relatives), demonstrating a culture of avoidance of financial intermediation.

Significance of working capital SMEs. Since reduction of costs has become a fundamental business requirement and it is not an attractive source of competitive advantage anymore, by now strong WCM is another way of improving performance of business (Farkas, 2004). Inventory, accounts receivable and accounts payables are primary aspects to WCM. Each component of WCM consists of two dimensions- time and money. Time can be referred as money when managing working capital is needed (Balakrishnan, 2011). Inventory and liquid assets management, crediting policy of firm — as a focal point of WCM- help enterprise to avoid investments in assets that will lead to small or no incomes at all (Dorisz, 2012).

Working capital is primary health indicator and the lifeblood of all businesses. In other words, working capital can be referred as a ‘fundamental to measure the welfare of business and a company`s ability to survive and prosper’ and difference between the monetary value of current assets and liabilities. Both the liquidity and profitability of companies are significantly influenced by the efficiency of working capital management (WCM). Depending on balance between them net working capital can be positive or negative. Overall, the bigger margin between current assets and current liabilities, the better business can be able to pay the invoices as they come due (Halkola, 2014)

Having more cash inflows than cash outflows is an ideal business cycle. In a simple case, availability of funds to pay creditors on time is sign of working capital`s health. When business cannot do this, companies face problem of crises of cash which will lead to downfall. To overcome this problem effective WCM is needed. Cash management is critical to survival of company, since access to liquidity is restricted in a credit crunch environment. The working capital`s effect is real and immediate and, it is totally unforgiving, if mismanaged (Kapadia, 2014). Effective WCM is particularly important for small and medium-size enterprises (SMEs), since external finance is their main source of current liabilities and most of their assets are in the form of current assets (Banos-Cabellero et al, 2010).

Although working capital is concern of all businesses, in practice, WCM should be seriously addressed by for SMEs. Current assets constitute most of SME`s assets, research results indicate that inventories, receivables and cash are responsible for up to 50 % of total assets in manufacturing companies, while because of financial constrains and difficulties to obtaining funds in long-term capital market current liabilities are main source of external finance (Decman, 2012; Banos-Cabellero, 2010). Thus capital budgeting and capital structuring issues are relatively low, in the context of SMEs, WCM is important part of capital budgeting.

SMEs tend to be more dynamic and agile, in the period of turbulence more vulnerable at the same time. It is due to less diversification in their activities and fewer financing options than their larger counterparts who have larger purchasing and selling power (Koralun-Bereznicka, 2014). Peel et al. (2000) points out that along with relatively high proportion of current assets and less liquidity, having volatile cash flows and reliance heavily on short-term debt are another features of SMEs.

Binks (1996) points inadequate long-term financing which leads to the need to rely to a large degree on owner financing and poor financial management out as primary culprit of failure among small enterprises in UK and US. Assessments of Organization for Economic Co-operation and Development (2013) indicate limited access to bank finance as a major obstacle to SME growth in Central Asia. Due to a high perceived risk and transaction costs for the bank, in Central Asia banks remain reluctant to lend to small firms. In this region only 20 % and 27 % of small and medium firms respectively use bank loans for their investments. Similarly, lack of working capital is cited as one of the top five short-term constraints for SMEs in the survey of Small Business Council, UK. It is not welcoming situation when business can not meet current obligations because of lack of liquidity (Padachi, 2013).

Many enterprises fail owing to mismanagement of working capital despite having healthy operations and profits, so it is a research theme that deserves increased investigation and especially for the SMEs as it is the wide belief that they are an essential element of a healthy and vibrant economy.

References:

- N. Pardabekova, E. B., 2012. Условия развития малого бизнеса и частного предпринимательства. AgroIlm, 1(21), p. 82.

- Karimova, D., 2012. Малый бизнес определяет социальную стабильность. Рынок, деньги и кредит, 10(185), p. 23.

- Zokirov, S., 2015. Kichik biznesning yorqin istiqboli. Xalq so`zi, 13(6196), pp. 1–2.

- Turaboy Koraliev, N. O., 2014. Growth of SME sector and ways of improving access to financial services in Uzbekistan, Tashkent: Tashkent Financial Institute.

- Manzurova, N. U. I. a. U. M., 2012. Small Business and Enterprineurship- Important Factor for Creating Employment and stability of Income (in Russian). Vecherniy Tashkent, 188(12.249), pp. 1–2.

- Farkas, A., 2004. Benchmark of Working Capital Performance, Budapest: Institute for Entrepreneurship Management.

- Khalmurzaev, N. A., 2000. Small and medium-sized enterprises in the transition economy of Uzbekistan: conditions and perspectives. Central Asian Survey, 19(2), pp. 281–296.

- Organization for Economic Co-operation and Development, May 2013. Improving Access to Finance for SMEs in Central Asia through Credit Guarantee Schemes, Private sector development: Policy Handbook

- Sonia Banos-Cabellero, P. J. G.-T. P. M.-S., 2010. Working capital management in SMEs. In: Accounting and Finance. s.l.:Wiley-Blackwell, pp. 511–527.

- Binks, M. R. a. E. C. T., 1996. Growing Firms and the Credit Constraint. Small Business Economics, Volume Vol. 8, pp. 17–25.

- Nikolina Decman, I. S., 2012. Liquidity management in Small and Medium-Sized Entities, International Conference of the Faculty of Economics Sarajevo.

- Organization for Economic Co-operation and Development, May 2013. Improving Access to Finance for SMEs in Central Asia through Credit Guarantee Schemes, Private sector development: Policy Handbook.

- Halkola, T., 2014. Improving Inventory Turnover and Working Capital Management by Business Model Innovation, Tornio: Lapland University of Applied Sciences.