Non-State education system has been established over the past 30 years. It has been contributing a significant part in the education socialization process according to the guidelines of the State. The aim is to provide education and training services for society as well as to provide high quality labor force for industrialization — modernization process, sustainable development, adaptable to today’s wide and deep international integration. Thus, non-state education system in Vietnam need to have suitable directions and to have enough good a management system in order to use any sources available in non-state universities. In fact, internal control system of non-state universities in Vietnam is still limited, weak therefore, within this study’s scope, we want to evaluate the current status of internal control system in non-state universities, thereby it helps the managers in newly-established non-state universities and other individuals in building the internal control system process.

Key words: Internal control system, non-state universities

In market economy and in the context of extensive economic integration today, training activities in non-state universities (NSUs) are also influenced by the rules of market economy, especially supply and demand rule, value rule…. NSUs education model wa born under the requirement of thinking renovation, NSUs work as an enterprise model but work for non-profit purpose. Under these requirements, NSUs have to suffer from much competition. Thus, to overcome these pressures, NSUs are required to catch the opportunities, in the market with a lot of education suppliers, NSUs must diversify their training forms, national and international training cooperation, etc in order to improve the quality of education to attract and provide the best educational services for learners, enhancing the value of profits, thereby increasing the reinvested value for other activities of NSUs. So, reforming management system in NSUs, specifically internal control system is necessary. Therefore, a strong and reliable internal control system will help NSUs to minimize the risks in their operations, we use qualitative methods of analysis to summarize, systematize publications related to the internal control system domestically and abroad. And then, based on various assessments in practice in NSUs of Vietnam. The NSU list of Vietnam today includes 64 universities, such as Thang Long University, Phuong Dong University, Hanoi University of Business and Technology, Binh Duong University, East Asia University, Thanh Tay University, Dai Nam University, Duy Tan University. These are non-state universities with a long history and much experience in research, training, which is is justified in training major and the number of students. So, building an internal control system is one of the pressing issues in the context of international integration, the level of competition is stronger and stronger … we want managers, those who in need to learn about internal control system in NSUs, which helps readers understand the importance of internal control systems from theory to practice.

-

Real situation of internal control system in non-state universities

- An overview about internal control system

The concept of internal control began to be used more in the early twentieth century in the field of auditing. In 1985, the United States National Council against Fraudulent Financial Reporting (commonly called Treadway Commission) was established and has since formed the Committee of Sponsoring Organization — COSO. According to COSO’s viewpoint about internal control system:

“Internal control is defined a process, effected by an entity’s board of directors, management and other personnel, designed to provide reasonable assurance regarding the achievement of an organization's objectives in operational effectiveness and efficiency, reliable financial reporting, and compliance with laws, regulations and policies (COSO, 2013).

The COSO’s concept of internal control is used and developed in many fields. In the public sector, internal control is an object attracting special attention by the state auditing. Some countries such as the US, Canada, the UK has taken the use of standards of internal control systems for administrative organizations such as the auditing standards of the General Accounting Office of the US government (GAO) in 1999. This standard refers to specific internal control in the administrative organizations and gives out five elements of internal control including provisions on the environment control, risk assessment, control activities, information and communication, monitoring. In the guidance for internal control standards of the INTOSAI (International Association of Supreme State Audit agencies) defined the concept of internal control are as follows: (INTOSAI, 1992):

The concept of internal control system of COSO and INTOSAI both confirm that in public sector, internal control systems are also understood as a process dominated by managers and the staff of the unit, is designed to provide a reasonable assurance to achieve the following objectives: the effectiveness and efficiency of operations; The reliability of financial report; Compliance with laws and regulations.

2.2 Basic elements of the Internal Control systems in the non-state universities

Internal control system in non-state universities is a system that includes elements to perform during management process of managers, to control the operation of the unit. In economic organizations in general, the non-state universities in particular, the internal control system includes the following basic elements:

2.2.1Control environment

Control environment described the attitude, the views of the managers of non-state universities towards the inspection and control, staffing and capacity of the personnel system. Control system creates different management shades in non-state universities in Vietnam at present. Essentially, control environment creates ethical forms and labor discipline of personnel at non-state universities, the elements of the control environment includes:

First; management philosophy and style of manager

Express personality, style of manager at non-state universities. If senior managers in NSUs think that internal control system is important in supervising the operation of the school, it represents the sobriety and ethical values of the manager, they need to develop ethical standards and behave properly, managers need to set an example for subordinates of the relevant department at the school to comply with such standards. In NSUs, the Board of Management and Managing Board are aware of internal control system function required for the inspection and surveillance of activities in schools, from that building internal spending rules, building regulations on organization and operation as a basis for implementation and control of activities. Conversely, if the members of Board of Management and the Managing board think that Internal Control is not important, it mean that they do not pay adequate attention to the Internal Control System. Hence, the result is that internal control system is only on paper and does not come into reality, leading to university’s unexpected aim and task.

Second, the ability of the staff and teachers

The ability of the staff and teachers contains the level of understanding and essential working and teaching skills to ensure the work is done with discipline, honesty, economy, efficiency and effectiveness, as well as to have a proper understanding of the responsibilities of each individual in the establishment of internal cotrol. In order to ensure that all members have the necessary of knowledge and working skills to complete the tasks, the university management should clearly identify ability requirements for a certain job, and it specifies the requirements for knowledge and skills so that individuals can be arranged right job with trained professionals.

Board of Management, Leadership and staff need to have enough qualifications to understand the development, implementation and maintenance of internal control, the role of internal control as well as their responsibilities in the implementation of general university’s mission. At the same time, every individual in the university needs to be aware of constantly improving qualifications, professional experiences to be able to meet the increasing requirements of the job, because every individual in an organization is an important chain to create a completed internal control. Board of Management, Leadership, staff and teachers also need to have the necessary skills to assess risk. The assessment of risk ensures that everyone can complete their assigned responsibilities.

In addition, managers need to raise awareness to individuals to help them understand their contribution in achieving the objectives of the organization and understand its importance in operating the internal control system effectively. Training is an effective way to improve knowledge and develop skills for the members of the organization. One of the training contents is directing the targets of internal control and methods of resolving the encountered situations at work.

Third, the organization structure

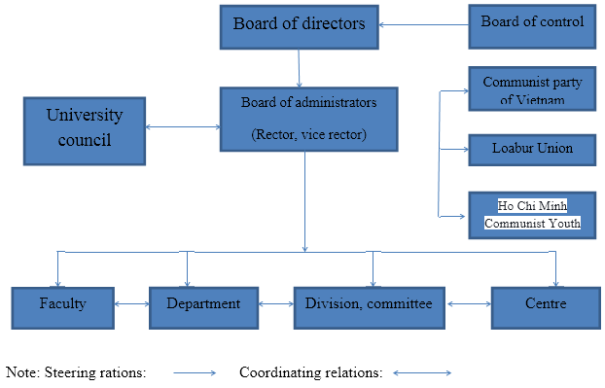

A streamlined structure in NSTs will ensure the execution of tasks thoroughly. The organizational structure is designed to prevent the violation of the rules of internal control and to eliminate inappropriate activities. Activities considered inappropriate are the ones that their combination can lead to the violation and hidden mistakes and fraud. The organizational structure consists of the division of authority and responsibility of the report and the appropriate reporting system. The organizational structure also includes internal audit department, the supervisory board, parts of inspection that is organized independently with the auditing objections and reported directly to the top leader in the NSTs. The organizational structure at the NSTs in Vietnam is organized as follows:

– Board of Management, the sole representative of the ownership of the NSTs in the development and orientation of the university, and in the decision of the key issues such as the organizational apparatus, personnel, finance and property.

– Council for Science and Training, a collection of individuals, including the principal, the vice- principals, members of the board, the head and the deputy of training department at the NSTs and other scientists in or out of the university join the Council in order to have tasks of the resolution on strategic goals and plans for development of the university, the resolution on the draft regulations on the organization and operation of the school or the regulatory amendments before the competent authority for approval.

– Administrators, principal and vice-principals. Principal is a legal representative of the university, directly responsible for the management and administration of the university's activities under the provisions of law. The principal has the right to enact and repeal the rules within the university to ensure the management, inspection and supervision of all activities of the university in accordance with the current regulations; recruiting and training teachers, officers and staff of the university. The Vice Principals help the Principal in the management and administration of university’s activities, directly in charge of a number of working areas assigned by the Principal.

– Functional departments, that is tasked to advise and assist the principal in the management, synthesis, recommendations, implementation of major areas of work of the university: hành chính- tổng hợp, tổ chức cán bộ, undergraduate and graduate, science and technology, political work management trainees, the accounting and finance, international relations and inspection.

– Faculties and departments. Faculties are the basis of administrative units of the university with the task of building the programs and plans for teaching, learning, compiling textbooks and organizing training process for one or several subjects; organizing scientific and technological activities; exploring the international cooperation projects actively; collaborating with science and technology institutions, production and business facilities, linking training with scientific research, production, business and social life. Departments are responsible for the content, quality, schedule of teaching and learning some subjects in the program and teaching plans as a whole; constructing and completing teaching contents and programs; compiling textbooks, reference materials related to training specialties and subjects assigned by faculties; conducting scientific research, developing technology and supplying some science and technology services following the university’s plans; actively cooperating with educational institutions.

Fourth, personnel policy

Human resource policy is the entire management methods and regulations related to staff such as employment policy, training, coaching, education, assessment, salaries, appointment, bonus and welfare and discipline. Each individual plays an important role in the internal control. The ability and confidence of personnel officers are essential to control effectively, so how to recruit, train, educate, assess, appoint and reward or discipline is an important part of the controlling environment.

Human resource management is also an important role in establishing the controlling environment by developing professionalism, enforcing transparency in daily work. Universities should issue regulations on recruitment, as well as the requirements, build up the description of required work for each position in the university to be able to manage staff, appoint the right person, right job.

Personnel policy has a significant impact on the existence of the controlling environment through the impact of other factors in the controlling environment as a guarantee of competence, integrity and ethical values.

Fig. 1. Organization Map of a non-state university. Source: The author’s survey

Fifthly; external control environment is the impact of the international economy, especially the legal documents that affect the non-public universities such as the accounting law (2003), higher education Law (2012), Decision 70/2014 / QD-TTg promulgating the regulations of universities issued on December 10, 2014 by the Prime Minister, and other regulations,...

2.2.2 Accounting information system

In the non-public universities, one of the fundamental elements of the internal control which has an important role in controlling the activity is accounting information system. Accounting apparatus in the non-public universities in Vietnam today is internal control; or Finance and Accounting performs the function of advising and assisting the Board of Directors, Board of Administrators in the field of management of finance, asset, accounting, and centralized management of resources,... according to the regulations issued by the State. Therefore, the accounting apparatus in these universities can be organized according to either the concentrated apparatus or the dispersed one. As the training scale of the current non-public schools are organized in the small form, accounting apparatus in the concentrated form may facilitate the the board of directors and administratiotors efficiently. In addition, the non-public universities currently apply accounting regulations 48 / 2006 / QD-BTC on April 19, 2006 by the Minister of finance to ensure the simple and economical nature. The use of document system in these universities is in line with the operational characteristics of the non-public ones. Documents are an important factor in the operation of the accounting and are used to control the activities of the organization effectively. In addition to the forms of required documents, the non-public universities also use some other documents,...

– Accounting document system; The schools have constructed specific rules about rotation sequence for each type of document used at the unit. Before documents are used, they have been checked by accountants in charge of administration. For the operation that requires the approval of the chief accountant, the documents have been signed by him. The content of the inspection of documents includes the legality of operations, accuracy of information, the adequacy of the signature, and the record transactions in the documents.

Archiving accounting documents in the non-public universities is also in compliance with the regulations of the current regime. After the documents have been recorded, they are filed and stored each month, and preserved according to the specified deadlines. However, the number of documents, especially the charge receipts and disbursements, in the universities is usually very large, leading to the fact that there should be a big storing place for them. Due to objective conditions of some schools, the documents are stored in the conditions which are not good, causing difficulties for the inspection and check when necessary.

–Accounting account system; The non-public universities now have built a system of accounts of their units on the basis of the unified system of accounting accounts for small and medium-sized enterprises in accordance with Decision 48/2006 / QD-BTC of the Ministry of Finance. Depending on the characteristics and size of each school, the number of accounts the schools use is different. beside the provisions of the accounting system, the opening of the detailed account in the non-public universities is very limited at present. Most of them stop at the opening of the detailed account at level 2, level 3 according to the regulations.

– Bookkeeping system; today the non-public university institutions organize accounting books in the form of general journal. However, for those using accounting software, types and forms of books may not entirely be in accordance with the rules of book system for each form. For those which have not used accounting software, the ledger system usually complies with the regulations of each different accounting forms basically. Because most non-public universities have used accounting software, the recording in the accounting books is automatically made (for those which have not applied the accounting software, they make the recording with a computer), mitigating the workload for employees and helping them find it easy to fix accounting errors that may occur.

– Reporting system; Under the rules of the current financial accounting system, the non-public universities have to establish financial reporting and tax settlement reports sent to the State management agencies in the end of each accounting year. They have to make the following types of reports now: balance sheet of arising accounts; balance sheet of Accounting; Business Report; Statements of cash flows; Notes to the financial statements. The schools have complied with the required system of financial reporting. However, these reports are mainly made in the mandatory and procedural manner, meaning that not much information is provided and deadline established is generally slower than required.

2.2.3Risk assessment in internal control system

Risk assessment is important in determining the possibility affecting the objectives of the universities. The goal is related to both the financial targets and non-financial ones. The analysis of the risk assessment will not help the schools avoid all risks but help them to limit the risks at an acceptable level. The process of risk assessment often includes:

Determine the targets: the targets may include financial and non-financial goals. The specific or general nature of the objectives is built on the basis of the operation of each school, and the requirements of each era. The financial goals of the non-public universities in Vietnam are usually balanced in relation to the objectives of the quality of training, the scale of training and the degree of human contribution to the society.

Identify risks: It means identifing risks and relation to each target. Risks can include internal and external risks across the entire operation or in each single operation. Risks can come from the following fundamental reasons:

– The changes in the rules of the organization's operating environment or the changes in senior personnel in the Board of Directors and Board of Administrators, the Council and the management of the department in non-public universities;

– The adjustment of internal information systems in the universities;

– —The rapid growth of the scale of the training fields, the increasing number of specialized training;

– The reorganization of the units held to support training and the rearrangement of extensive specialized training or the deletion of specialized training;

– Domestic and international Join Training;

– Application of new accounting principles;

Analyse and assess risks: determine the frequency of risk and the level of risk on the basis of risk assessment criteria so that risk management approach will be proposed to deal with the risk if it occurs during the development of the school.

2.2.4Internal control activities

Control activities in non-public universities are policies and procedures established to deal with risks and guarantee the achieviement of goals and tasks of the unit. Control activities exist in all departments and all levels of the organization in one unit. To achieve effectiveness, control activities must be appropriate, consistent between periods, efficient, easy to understand, reliable and have a direct link to the control objectives. Control activities are available throughout the organization, at different levels and functions.

In terms of purpose: control activities include prevention control, detection control, offset control

– Prevention Control: policies and control procedures are taken to prevent and minimize the possibility of errors or fraud, affecting the achievement of the objectives of the unit.

– Detection Control: policies and control procedures are designed to find out errors or acts of fraud that have been made timely.

– Offset Control: other control procedures are offered to replace the weak and inefficient control activities.

In terms of Function and action of control included

–Decentralization and approval

Implementing of the transactions is made by an authorized in his or her responsibilities and powers. Authorization is a main way to ensure that only valid incurred transactions are approved by the manager’s desire. Authorized procedures must be documented and clearly transmitted with the specific conditions and terms. Complied with the authorization’s regulation means that employees must act following the guide in the permission limit of the leader and the law

–Control the processing of information and transactions; Control the information processing plays an important role in controlling operations, in general. When controlling the process, the unit needs to ensure that the system of vouchers and documents must be strictly controlled and the type of transactions must be properly approved. Therefore, controlling the processing of information including;

General control; is the operational control applied to all application systems to ensure these systems operation continuously and stably;

Independent checking the implementation; independent checking is to be checked by individuals with other individuals who are operating the transactions. The requirements for these individuals are to check the others independently in order to improve the objectivity in the implementing process. The transactions and events must be checked before and after treatment.

Analysis: this operation is to review the finished work by comparing the implementing results and the estimation data or the financial information with non-financial information in order to find out unusual fluctuations for managers having with in time adjusted solution.

The analytical methods include:

– Comparison: the documents are compared with the appropriate vouchers periodically, such as records of bank deposits compared with bank statements

– Review the implementation of the operation: the implementation of the reviewed activities based on some standards, basic principles, effective evaluating and effectiveness. If the review shows that the activities implemented to achieve these objectives, it needs to be reviewed to make the necessary improvements.

– Review the administration, handling and operation: the administration, handling and operation should be reviewed periodically to ensure they follow the principles, policies, procedures and other recent requirements.

– Monitoring employees (allocate work, review and accept, guide and train): monitoring carefully helps to ensure the goals of the organization which will be implemented. The allocation and acceptation the work employees include:

– Noticing clearly, obligations, responsibilities and explanation of each employee.

– Appreciating work systematically of each member in the necessary scope.

– Accepting work following the standards to ensure that work is implemented in correct orientation.

– The managers give employees the necessary guidance and train them to ensure that errors, waste and wrong action reduced to minimum.

When a control operation is implemented, it is important to ensure the effectiveness obtained. Therefore, action overcame the consequence is to complement necessarily to control operation in promoting the role.

- Conclusion

In terms of nature, KSNB systems in the non-public universities clearly expressed the policies and control procedures. Policies and control procedures will be developed and operated on its background is the control environment and accounting information systems. Policies with control procedures will only ensure the effective and continuous operation through the process of evaluating risk and monitoring. Therefore, to ensure operating efficiently and implementing social goals, the non-public universities in Vietnam today with building KSNB systems must pay attention to both factors presented above, the research was implemented and analyzed by qualitative methods. Thus, the gap of research is the potential risk and the risk in building internal control systems in the non-public universities in Vietnam today.

References:

- Nguyen Thi Hai Yen, MA. (2016) Improving the internal control system in public universities of Vietnam in the context of the implementation of autonomy. Scientific Journal of Auditing Research.

- Nguyen Huu Dong (2009), accounting information system in universities in some countries in the world and lessons for Vietnam universities, Journal of Economics and Development, (Vo 2), November 2009.

- Nguyen Huu Dong (2010), Improving financial management mechanism and process of accounting of expenditures in the public universities, Journal of Economics and Development, (156), June 2010.

- The Socialist Republic of Vietnam (2005), Resolution 14/2005 / NQ-CP on the comprehensive and basic renewal of Vietnam higher education in the period 2006–2020.

- COSO (2013), Internal Control — Integrated Framework, http://www.coso.org/documents/Internal %20Control-Inte- grated % 20Framework.pdf

- The Prime Minister of The Socialist Republic of Vietnam issued Decision No 70/2014 / QĐ-TTg on the Conduct of Universities, December 10, 2014.