Commitments in the context of the modernization of the economy, including joint-stock companies and limited liability companies, focusing on the organization of the internal audit service. As can be seen from the Cabinet ministers of the Republic of Uzbekistan adopted 215th resolution “Regulation about internal audit service in entities” in 2006, October 16 [1] on the basis of the internal audit service, and the value of assets balance of $ 1 billion. The company worth more than the introduction of the obligations of the Internal Audit Service (Table 1).

Table 1

The value of assets of one billion dollars. worth more than [5], the implementation of internal audit in enterprises

|

№ |

Areas |

2007 y. |

2013 y. |

2014 y. |

2015 y. |

2015 account changes in% compared to 2007 y. | ||||

|

on practice |

% |

on practice |

% |

on practice |

% |

on practice |

% | |||

|

1. |

Republic of Karakalpakstan |

22 |

6,3 |

24 |

5,0 |

8 |

4,0 |

6 |

3,2 |

-3,1 |

|

2. |

Andijan |

29 |

8,3 |

20 |

4,2 |

19 |

9,4 |

11 |

5,9 |

-2,4 |

|

3. |

Bukhara |

14 |

4,1 |

37 |

7,8 |

4 |

2,0 |

5 |

2,7 |

-1,4 |

|

4. |

Jizzakh |

5 |

1,4 |

23 |

4,8 |

15 |

7,4 |

6 |

3,2 |

1,8 |

|

5. |

Kashkadarya |

37 |

10,6 |

33 |

6,9 |

13 |

6,4 |

10 |

5,3 |

-5,3 |

|

6. |

Navoi |

16 |

4,6 |

17 |

3,6 |

11 |

5,4 |

8 |

4,3 |

-0,3 |

|

7. |

Namangan |

11 |

3,2 |

25 |

5,3 |

15 |

7,4 |

6 |

3,2 |

- |

|

8. |

Samarkand |

28 |

8,0 |

43 |

9,0 |

12 |

5,9 |

9 |

4,8 |

-3,2 |

|

9. |

Surkhandarya |

35 |

10,1 |

33 |

6,9 |

9 |

4,5 |

8 |

4,3 |

-5,8 |

|

10. |

Syrdarya |

16 |

4,6 |

13 |

2,7 |

9 |

4,5 |

9 |

4,8 |

0,2 |

|

11. |

Tashkent region |

22 |

6,3 |

37 |

7,8 |

24 |

11,9 |

22 |

11,8 |

5,5 |

|

12. |

Fergana |

31 |

8,9 |

43 |

9,0 |

13 |

6,4 |

13 |

6,9 |

-2 |

|

13. |

Khorezm |

33 |

9,5 |

19 |

4,0 |

6 |

3,0 |

6 |

3,2 |

-6,3 |

|

14. |

Tashkent city |

49 |

14,1 |

107 |

22,4 |

44 |

21,8 |

68 |

36,4 |

22,3 |

|

TOTAL |

348 |

100 |

476 |

100 |

202 |

100 |

187 |

100 |

- | |

According to the table above, can greatly improve the performance of joint-stock companies and the introduction of modern methods of corporate governance reforms were terminated as a result of a number of low-profit joint-stock companies and foreign investors in 2015 as a result of a drop in sales of companies, approved by the Internal Audit.

Internal Audit Service during the audit to verify the elimination of violations of legislation and of financial and economic activity of the company on the measures taken to improve the effectiveness of evaluations.

At the end of each quarter, and the company's Supervisory Board will receive a report on the results of audits of the Internal Audit Service, to address identified deficiencies and improve the efficiency of financial and economic policies of the company.

Performs internal audit, as well as the types of services, analysis of production and a detailed study of these options would better clarify the ways in which the development of other industries. Thus, the work of all the strengths and weaknesses of its assessment of the strength of current conditions, as well as determining the prospects of development of the country.

Nevertheless, the company always steps in this policy and understand full or in progress. Enterprise managers to identify deficiencies in the implementation of these and for a sufficient amount of time. This is the complete omission of the Internal Audit Service. This service is available every day, experts or their work, because of the activities of the entire management system leads to serious errors, losses, error calculations, to protect the weak and can break or decline in business activity will help you to identify the weaknesses to realize their full potential.

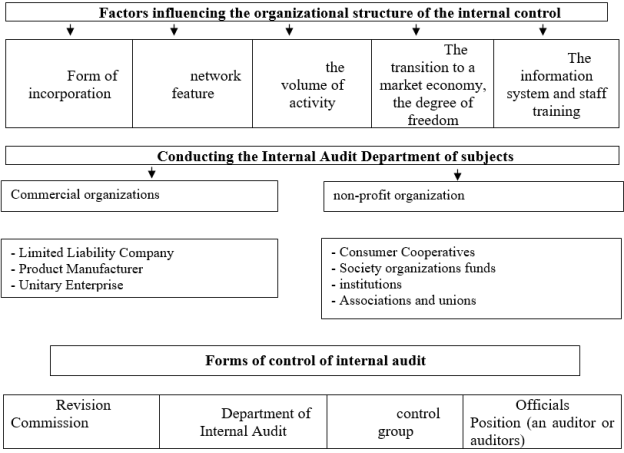

Fig. 1. The organizational structure of the Internal Audit Service

At the same time, it should be noted, does not operate to monitor and verify their function, they are still part of personnel. They are all about the senior management of information and discuss their routes on a regular basis, and because of this, the accuracy to shape their own tariff plans and prospects for the future. The administration of the enterprise communications to help organizations improve the quality of management will be able to provide more detailed information. Based on the above, internal audit, in order to improve the financial position of the enterprise, to achieve effective results, as well as the legitimate conduct of financial control measures.

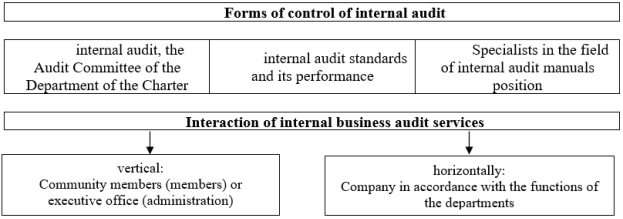

Following an internal audit of the internal audit should provide rules: Internal Audit Charter, job expert instruction, specialists of the department and its business plans, guidelines, audit, internal audit standards, internal audit rules, the methodology of the internal audit and the audit evidence guidelines, audits and the results of the implementation of the guidelines.

Aimed at ensuring the achievement of the objectives of the internal audit is a management control tool. The results of the analysis to guide the internal audit to assess the effectiveness of a particular department, providing advice and information.

The results of the internal audit of the company management, taking into account the limited resources available, as well as labor laws, and is also used to carry out this work.

The Internal Audit Service Internal Audit Department plays a key role, he will be in direct contact with the Supervisory Board of bilateral interest. The head of the internal audit, financial reporting, as well as other issues related to the company's Supervisory Board will be appropriate to participate in the meeting. Plans to take part in these meetings, the head of the internal audit department and ensure the exchange of information on the activities of the division between the other departments increased [2. P. 54–55].

The Internal Audit Department periodically about half the production cost of the work carried out and an oral or written report to the Supervisory Board, the management of each year audit work plans of the US Department of distribution plans and cost estimates. Department identified during the audit, as well as information on all the facts that may cause harm to the organization. This indicates improper, unlawful acts, errors, inefficiency, expense, unprofitability conflict of interest, and may be due to lack of control. The head of the company selects the appropriate steps to remedy the identified deficiencies. In addition, the head of the service obligations of groups and their control, the results of implementation of the recommendations of the audit process for the audit, if necessary, the financial analysis and advice on specific issues, administration orders order of supervision and enforcement, as well as prepare a report on the work carried out by the internal audit.

The Internal Audit Department is responsible for the provision of audit control. aspects of the audit function in the management of a continuous process of elimination planning, staff and management are approved to audit programs provide convincing evidence that the auditors and the results of the working documents with the approval of the control reports. Audit reports are objective, clear, meaningful and timely audits to ensure that the objectives are achieved. Documented evidence of control. The level of control required experience of internal auditors and the audit related to the complexity of the problem.

Internal auditors Group has adopted the following:

– Order of implementation of the work plan and schedule;

– The shape of the control group and the auditors;

– The master plan and develop the internal audit program;

– The structure of the internal audit report and the audit results, which could affect their harmful consequences for the service manager;

– Acts which are directly involved in the preparation of the results of the audit processes and documents and systematization;

– The results of the report on the results of the internal audit and management to seek adoption of resolutions;

The group of auditors -internal comments on the file size and time organizes and controls.

The audit practice is essential for the understanding of the situation in which it appears. This is an opportunity to apply the knowledge in case you want to avoid or detect potential problems and help them to be analytical and rational decisions. Internal auditors are fair, employees know and work with them, as well as the evaluation of the evidence found in the recommendations made orally or in writing, should be clear.

Necessary service experts of internal audit and their specific requirements. State enterprises as an expert, different areas of accounting and auditing in the field of sufficient knowledge, experience and professional skills, which can answer questions in this area. For example, the expertise of contracts, constituent documents, interpretation of the legislation and legal assessment to determine the value of property types and can be used to determine the volume of work performed, and other. Unfortunately, the internal audit standards clearly define the work of the expert, so that it can be used as a model for the external audit standards. It can be changed according to the characteristics of the internal audit. Expert of the Internal Audit Service carried out by the company or on behalf of the audit object, in accordance with the recommendations of the audit team management contract. Formalized in writing the results of the expert examines the internal audit service and a part of the working papers.

In practice, each organization department of internal auditors or result came from the service.

Based on the above, the internal audit department should pay attention to the operation as follows:

– first, offering better control over a particular industry or an affiliated company;

– second, scheduled and unscheduled inspections and monitoring to determine the most important aspects of the development, production resources allow;

– third, incentives, internal auditors in many cases, the company, its subsidiaries and divisions, as well as several other members of the economic and analytical services can provide expert advice and ratings.

References:

- Cabinet ministers of the Republic of Uzbekistan adopted 215th resolution “Regulation about internal audit service in entities”. 16 October 2006 year.

- Андреев В. Д. Внутренний аудит. Учеб. Пособие. — М.: Финансы и статистика, 2003. — 464 с.

- Евдокимова A. В. Внутренний аудит и контроль финансово — хозяйственной деятельности организации: Практическое пособие. — М.: Дашков и К, 2009. — 208 с.

- Пугачёв В. В. Внутренний аудит и контроль. Организация внутреннего аудита в условиях экономического кризиса: учеб. — М.: Дело и сервис, 2010. — 224 с.

- gki.uz (The State Committee of the Republic of Uzbekistan for Privatization, Demonopolization and Development of Competition)