There is no doubt that one of important indicators of the economic performance of a country is the business activity. Current age can be characterized by increase development of business, its diversification and going global. For making companies successful managers need to effectively evaluate the proposed investment opportunities. Method of real options is thought to be one of the most effective tool for achieving that.

The article is relevant due to the fact that the theory of options provides an opportunity to allocate two groups of new possibilities contained in an investment project. The first of them — a possibility of changing parameters of the investment project with time. It can be expansion or reduction of the project, change of sources of raw materials or refusal of implementation of the project after obtaining additional information. The second group of opportunities considers the external side of the project, i.e. completing of one project makes possible to implement other project which would be impossible without finishing of the first.

The aim of the article is to examine the real options method and its applicability for the pharmaceutical sphere.

To achieve the posted aim it is necessary to complete the following goals:

– Analyze the nature of the real options

– Consider advantages of using the real option method

– Study and evaluate real options applicability in pharmaceutical sphere

– Analyze obstacles of using real options

The concept of options has arisen in the theory and practice of financial investment instruments and belongs to the section of derivative securities, which include options and futures.

Futures are the contracts having validity in which the seller undertakes the obligation to put financial or commodity assets at the fixed price in particular time, and the buyer of the contract undertakes to get them on these conditions. Options are the securities granting to the investor the right to buy or sell other securities or other assets at specially stipulated price during a certain term. Depending on the set investment object, it is possible to distinguish several types of options.

Historically the term «real options» had arisen after the methodology of application of the theory of Black-Scholes to real assets was developed. The concept of real options is based on the concept of financial options.

Financial option — the contract granting the right (but not an obligation) for purchase/sale of goods or a financial asset at in advance established price during a certain, in advance established period of time. They can be divided into Put and Call options. Put is an option for sale of a basic asset on a fixed rate before the expiration of the stipulated term. While Call is an option for purchase of a basic asset on a fixed rate before the expiration of an established period.

Real option — an option for which basic asset are real assets: plants, reserves of oil, car, production investments, etc. As it was noted earlier the concept of real options reveals new opportunities of investment project. The possibility in a broad sense of this word can have the cost, and at the same time, the more similar opportunities are contained in the project, the more costly this project becomes. When people speak about a possibility of the choice, they usually describe it in qualitative, subjective terms.

The concept of real options allows estimating quantitatively the opportunities, which are available in the project, and with doing that to include them in calculation of costs of the investment project. The quantitative assessment plays a key role at adoption of the investment decision, in most cases, when additional opportunities are estimated only qualitatively, intuitively, they simply are rejected when comparing quantitative parameters of the project and in the best case, they represent just additional pluses of the project with other things being equal. For a quantitative assessment, the concept of real options uses the same indicators, as the classical theory.

Cash flows characterize a quantitative component of the project. At the same time the more the cost of the expected cash flows, the more costly a real option becomes. Investment expenses are understood as quantity of money which will be necessary for implementation of the project. At the same time, the cost of a real option is inversely proportional costs of investment expenses.

Increase in time up to the expiration of a possibility of implementation of the project increases the cost of a real option as the owner of an option receives more (on time) opportunities to use properties of a real option.

The volatility characterizing variability of the prices is also directly connected with the cost of a real option. Usually high volatility means a high probability to receive increased profit, and at the same time to suffer heavy losses. However real options allow to limit losses and to keep a possibility of receiving additional profit that makes them more valuable in the conditions of the raised volatility of the prices.

It is possible to distinguish several types of real options:

– The option for the choice of time of implementation of the project can be used if the decision on the beginning of the main investments can be postponed. It allows management to define exact date in the future when it is necessary to begin the main investments.

– The option for refusal of the project. In methods of the traditional analysis of the project it is supposed that the project will be carried out during the whole considered time.

– Growth options are also among the most important elements of a corporate strategy. The option of growth is used when initial investments serve as a necessary condition of future development. At the same time, the current project can be considered as a link in a chain of the projects connected with each other.

– The option for implementation of consecutive investments arises when investments during the project are carried out consistently one after another and at the same time there exists an opportunity to interrupt the project at any stage in case of negative development of the situation.

Initially, for the estimation of real options costs were used formulas applied by Fisher Black, Myron Scholes and Robert Merton in their works about the valuation of financial options. Later on, in 1984 there appeared works of Stewart Myers “The financial theory and financial strategy” and Carl Kester “Options for growth today tomorrow”. This is considered to be a starting point in the development of practice of a method of real options application.

Nowadays, the theory of options develops in the direction of real assets. The method of real options considers methodology of hedging of the portfolios including not only securities, but also the investment projects assuming property investments in various assets. Real assets are any material assets, such as precious metals and stones, strategic raw materials, investment projects.

The model of real options gives managers an opportunity of planning and management of strategic investments and represents synthesis of an assessment of market value and adoption of investment decisions in the conditions of uncertainty.

Application of a method of real options to an assessment of investment projects is expedient when the following conditions are satisfied:

– the result of the project is to high degree of uncertainty;

– management of the company is capable to make flexible administrative decisions at emergence of new data during the project execution;

– the financial result of the project depends on the decisions made by managers. At a project assessment by a method of the discounted cash flows NPV value is negative or slightly more than zero.

The great practical example of use of options for implementation of consecutive investments is the pharmaceutical industry. All those characteristics mentioned above are met by any project undertaken in the pharmaceutical sphere. In pharmaceutical industry real options became relatively popular in the late nineties. Merck, one of the oldest chemical and pharmaceutical companies in the world, have been using real options since 1995 to evaluate such projects as, for example, the acquisition of a new technology from a perspective small biotech firm. And trend lead to the fact that nowadays most large pharmaceutical companies hire a real options specialist for their valuation teams. Production of new medicine demands carrying out several series of researches and tests. At the same time, the probability of final success increases in process of transition to a new stage of check.

From the point of view of investors the pharmaceutical industry is interesting by development of new drugs that will get to the market and be successful (the revenue of the drug should be more than $1 billion per year). Investment in the pharmaceutical industry is associated with slow return on their investments due to the time-consuming research and testing process (around 6–13 years including ~1½ years for approval and licensing). That requires the effective patent period, when the product is in the market, to be at least 7–14 years. Also investors deal with high level of uncertainty because only few drugs get approval from authorities. And according to the statistics only 1/5 of all approved drugs are bringing profit sufficient enough to pay off expenses. In pharmaceutical industry R&D costs are among the highest in the process of development a new drug. So the management of pharmaceutical companies are constantly monitoring the development of new drugs closely, and deciding on whether to abandon investment or continue, when the situation the market changes.

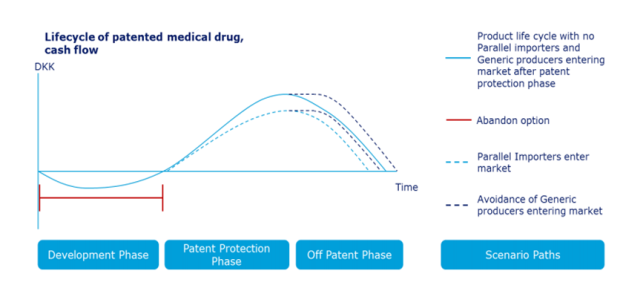

There are three major phases in the product life cycle of a medical drug: development phase, patent phase and off patent phase.

During the first phase the cash flows are always negative because company only spends money on R&D. The management is estimating time and expected costs before market launch. And because of uncertainty there are several different scenarios (approval of authorities, no approval or unpredicted unfavorable conditions on the market). So there is an option to abandon investment.

If the pattern is received, the drag goes to the market and generates positive cash flows. But the amount of those cash flows (high or moderate) also depends on different scenarios, for example, whether or not parallel importer enters the market. If the parallel importer enters the market the management has the option to set the different price that will keep cash flow at an optimal level.

Assuming projects reaches off-patent phase, cash flows (moderate or low) then depends on whether or not generic producer enters the market and potentially gain some market shares. Management has options to reduce, raise or leave price unchanged. The best strategy will be chosen based on the assessment of loyalty of customers.

Traditional corporate finance theory suggests that firms should use a discounted cash flow model (DCF). But described above example is shows that for this circumstances real options are better for decision making than traditional NPV method. DCF model requires precise long-term assumptions and considers only one scenario that evaluated project will be performed till the end. Real options allow considering several future scenarios. This more realistic modeling takes into account the possibility that the management will stop the projects to prevent further losses, will increase the size of a production operation in response to higher-than- expected levels of demand, or cut funding for a research project that is not inventing marketable products. This flexibility is very valuable for business.

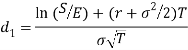

In order to estimate the value of an option it is necessary to determine five parameters, value of four of which are available to investors: S share price, the price of execution E, a risk-free interest rate r and an interval of time to the term of the expiration of an option T. The initial Black-Scholes formula was developed for estimation of value of financial options of Call type.

The formula looks as follows:

![]()

![]()

Where:

S — the stock price

E — exercise price

r — risk-free rate

T — time to expiration

— volatility

C — price of a real option

In case of research pharmaceutical project the main difficulty in implementation of real option method is estimation of listed above parameters.

– As a stock price the expected present value of the cash flows from the project (i.e., the DCF value) can be taken. It is this value that has the variation, or the probability distribution, associated with it over the multiyear period. That calculation is based on best estimate as to the cash flows which would be generated by the project.

– The exercise price can be the cost of building the facilities (i.e. plant) and costs associated with implementation of new technology.

– The time to expiration can be based on the expected time to develop the product and build plant.

– The volatility can be based on the annual standard deviation of returns for biotechnology stocks that has a similar level of risk as the evaluated project.

The risk-free interest rate is traditionally based on the prevailing yield on two- to four-year Treasury bonds.

However there is an opinion that real option method is more popular in academic sphere than in real business practice because of several problems arising during its implementation. First of all the applicability of a real options approach to strategic decision making depends on the extent to which the characteristics of the evaluated investment proposal match the assumptions of the option model. In practice it is more important to focus on differences between financial and real options than on similarities. Real options have not inherited some explicit features of exchange-traded options. For example, in the Black-Scholes formula, the stock price is assumed to follow a lognormal distribution, with a constant level of volatility. Over time, the distribution of stock prices gets wider, as the potential stock prices increases exponentially at the high end and asymptotically approaches zero at the low end. But this assumption may be inappropriate for a real option because it may ignore the product life cycle. Sales pattern may not follow lognormal distribution.

For example, Black-Scholes assumes that the longer some pharmaceutical company waits to exercise its option, the more valuable the option becomes. It is explained by the lognormal stock price distribution assumption and the fact that present value of the exercise price is lower for a longer option. However in reality the longer company waits to exercise its option, the lower the value of the project. This is because the significant value of the project comes from patent protection. Without the patent competitors are free to copy the drug formula. As the patent has a fixed expiration date, the longer company waits to exercise the option, the less time is left on the patent and the lower the overall economic value. So, the classic Black-Scholes model have to be adjusted to account for the negative effects of having to wait longer to exercise the option.

Nevertheless, there is a difficulty in calculating the model's inputs. If the inputs that are normally given for financial options are improperly calculated or estimated for real options, then the results from using the model will be incorrect. There is no observable “stock prices”, “exercise price” or “time to expiration” for real options in the form of research projects because the outcome of the research is unknown until the project is completed and project could be prolonged. It makes decision making very difficult at the time of the “expiration”. Also volatility is an often-cited input factor problem. Reliable sales forecasts are only observable within large companies that revalue on a regular basis their projects. In other situations this information is difficult to obtain.

And the last noteworthy detail is a risk-free discounting that is left from the financial options. The use of risk-free is a mistake because most investment projects and drug development in particular is risky. For them it is normally not possible to hedge the risk, therefore we have to use a discount rate that includes a risk premium.

Summing up, all described advantages of real options come along with relatively more complicated calculations than in case of traditional DCF model. And all errors mentioned above lead to unreliable or unrealistic results. So this approach should be used accurately and be tailored for particular circumstances of each evaluated project.

References:

- Assessment of innovative projects in pharmaceutical branch: Approach on the basis of integration of real options and indistinct sets/Rogova E. M., Siric E. S., HSE

- URL:https://www.hse.ru/data/2015/01/24/1105577256/ %D0 %A0 %D0 %BE %D0 %B3 %D0 %BE %D0 %B2 %D0 %B0-nyy %20(1).pdf

- Evaluating real options as a means for investment appraisal under uncertainty and its degree of utilisation by companies/ Andreas Würfel, 2003

- URL:https://books.google.ru/books?id=NdZ2AQAAQBAJ&dq=Black+F.,+Scholes+M.+(1973).+ %C2 %ABValuation+of+technology+using+real+options %C2 %BB.+Journal+of+Political+Economy&hl=ru&source=gbs_navlinks_s

- Real Options, Acquisition Valuation and Value Enhancement/Aswath Damodaran, 2012

- URL: http://people.stern.nyu.edu/adamodar/pdfiles/eqnotes/packet3a.pdf

- NYU Stern School of Business Chapter 8 Real Options

- URL: http://people.stern.nyu.edu/adamodar/pdfiles/valrisk/ch8.pdf

- Harvard Business School — Making Real Options Really Work/Alexander B. van

- Putten, Ian MacMillan, 2004 URL: https://hbr.org/2004/12/making-real-options-really-work

- Methods of analysis and assessment of efficiency of investment projects through real options, Moscow/ D. G. Perepelitsa, 2009

- URL:http://economy-lib.com/metody-analiza-i-otsenki-effektivnosti-investitsionnyh-proektov-na-osnove-realnyh-optsionov

- Real Options compared to traditional company valuation methods: possibilities and constraints in their use/Dzyuma U., 2012

- URL: http://e-finanse.com/artykuly_eng/220.pdf

- Real Options in the Pharmaceutical Industry (Valuation)/ Dr. Oecon Peter Ove Christensen; School of Economics and Management Aarhus University; 2013 URL: http://www.specialer.sam.au.dk/econ/2013/20063969.pdf

- Real Options Analysis and Strategic Decision Making/Edward H. Bowman; University of Pennsylvania; Gary T. Moskowitz; Southern Methodist University; 2009 URL: http://www.business.illinois.edu/josephm/BA549_Fall %202014/Session %207/7_Bowman %20and %20Moskowitz %20(2001).pdf

- Avance: Corporate Finance in Life Science — Real Options: Dos and Don’ts; November 2009 — № 9 URL: http://www.avance.ch/newsletter/docs/avance_on_real_options.pdf